What I learned from analyzing +10,000 public documents using AI.

It’s no secret the wine industry is in challenging times right now. It’s changing rapidly due to shifting consumer preferences, inflation, trade tariffs, climate change, and new competitors. In these uncertain times, global wine sales volume has been down 5% to 6% over the last 18 months, adding to wine industry worries.

With that context, I wanted to understand the strategic issues important to leading wine producers. To do this, I analyzed +10,000 public statements and reports from 25 large public and private wine producers from across the USA, Australia, and Europe, using an AI-based research platform.

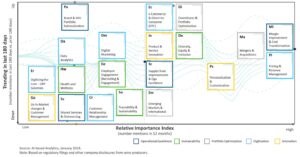

Here are the most important strategic issues in the last 12 months and how they are trending:

The analysis is split into ’Relative Importance’ based on the total number of mentions of the strategic topic in the last 12 months, and the percentage change in mentions in the last 180 days (’Trending’.) The AI helped interpret the strategic issues (e.g., Margin Improvement & Cost Transformation) to ensure adjacent terms were included (e.g., cost reduction, SG&A reduction, restructuring, etc.). What the analysis shows is there are four strategic issues – Margin Improvement & Cost Transformation, Pricing & Revenue Management, Mergers & Acquisitions, and Personalization & Customization – that are most important to wine producers today.

Let’s look at what the wine producers are saying about these four important strategic issues:

Pricing & Revenue Management

Pricing and revenue management is one of the most powerful levers for driving profitable growth and is top of the Executive agenda. Some of the trends we saw during COVID-19 are here to stay. Shifts in consumer preferences (private label, value retailers, decreasing loyalty, price transparency), and supply chain impacts have required wine producers to re-think their pricing strategy and execution.

For the last few years, the playbook for wine producers centered on price taking. Input costs rose dramatically, so price had to follow. Companies did all they could to control costs to limit pass-through, and premiumization helped justify what they charged. But the name of the game was price.

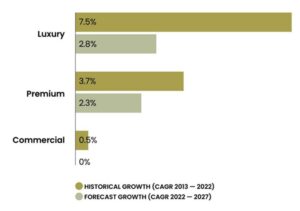

But the world is changing. Further significant price increases might not be possible in an uncertain economy where retailers are pushing back, consumers are unwilling to pay more, and competitors are becoming more aggressive on price. The shift to premium and luxury price segments will likely slow down and become less important as a growth driver in the future (see below forecast from IWSR).

Source: IWSR 2022, still and sparkling wine only, portfolio price points per IWSR segmentation, value growth shown

If price and premiumization have run their course, wine producers will need to pivot to volume. But not all volume is equal. Companies must pay renewed attention to execution, driven by a clear eye on profitable volume.

Margin Improvement & Cost Transformation

The pricing and premiumization challenges are exacerbated by rising costs of goods and labor, which are putting pressure on margins. While rising costs hit hard at any level, it’s the lower priced wines that are the most vulnerable. The increasing cost of glass, labor, cardboard, fuel to transport eat into profit. If you are going to make profit at that low end and still deliver a product that is quality, the trends are tough below $12 a bottle.

Wine producers are improving their margin by discarding poor performers. In 2022 and 2023, wine producers did a fair amount of SKU rationalization to free up production capacity and pruning away low-performing products and brands to increase the average mix margin. This trend of SKU rationalization will likely continue as a priority for 2024. More radical changes to mix involve divesting entire brands or lines of business as we saw with Constellation Brands selling five wineries and more than 30 U.S. wine brands to E&J Gallo. Improving supply chain performance was another key theme in transforming the cost base. Wine producers took measures to streamline supply chains, review grower contracts, and restructure operations. While the industry has tried to address supply chain challenges over the last few years, more progress is needed, and will likely be another focus area in 2024.

Mergers & Acquisitions

The challenging times are putting many wineries into a stress-test environment. Some brands are selling because financially, with margins tightening in the industry, they just do not have anywhere to go. Most small family wineries have an operating line of credit and when interest rates shot up to 8% or 9% last year, it became difficult to operate and make money. In the first half of 2023, the industry saw 11 major deals. The second half brought Duckhorn’s $400 million purchase of Sonoma-Cutrer, Treasury Wine Estates’ acquisition of Daou for up to $1 billion, and Gallo’s purchase of Rombauer and Massican in the USA.

High-interest rates may dissuade private equity investors, several of which use debt funding for acquisitions. That dynamic gives wine producers with strong corporate balance sheets an advantage when competing for deals. “Bolt-on” acquisitions is the phrase most used by executives in investor calls. However, vertical integration may help companies gain greater control of their value chain, ensure supply, and protect margins from input cost increases.

Personalization & Customization

With consumer preferences and consumption changing, how did wine producers grow loyalty among current consumers and reach out to new ones? Wine producers felt it was an important part of their strategic growth to create a more direct connection with customers and consumers enabled through owned distribution. In emerging markets, this was particularly important. Companies focused on converting consumers who already bought their brands from third-party retailers and transitioning their current Direct-to-Consumer (DTC) customers to a loyalty program or subscription service. Increasingly, personalized buying experiences that embrace shared beliefs are becoming an expectation.

Innovation in Personalization & Customization was focused on format, channel, and occasion. Enabling customization and transparency through tech is one way to evolve new customer engagement, such as embracing emerging technology to trace grapes from vineyard to glass, or creating an online-to-offline experience that maps to occasion-based purchase triggers.

I highlighted the four most important strategic issues for wine producers based on the relative importance. However, there are other issues that are becoming important such as e-Commerce/DTC, Product & Service Innovation, Diversity, Equity & Inclusion, and Divestitures & Portfolio Optimization, and I will cover these in another post on what’s going on in the wine industry.